TAXATION OF PARTNERSHIP PART 2

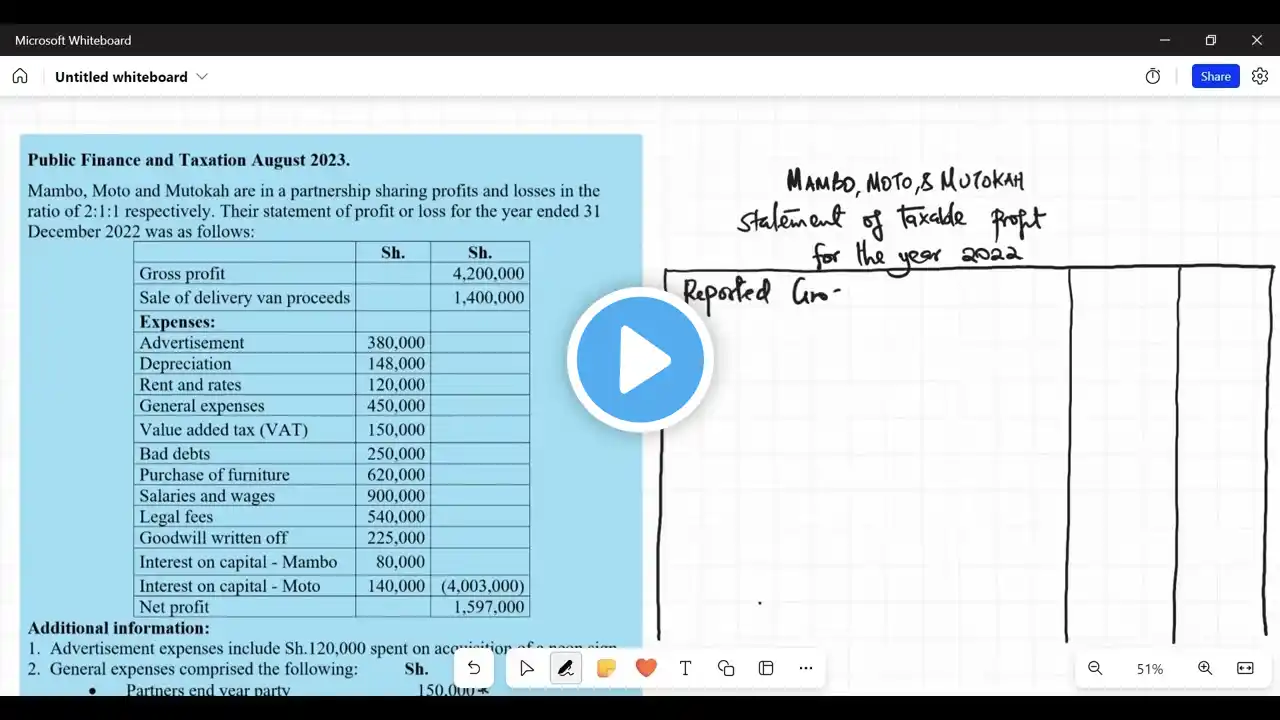

A worked example covering capital allowances, disallowed expenses and income to arrive at tax adjusted profit after capital allowances.

A worked example covering capital allowances, disallowed expenses and income to arrive at tax adjusted profit after capital allowances.