CBSE 12th Accountancy 67/1/1 2025 Set 1 Solved Paper Q24 Partnership Dissolution Journal Entries

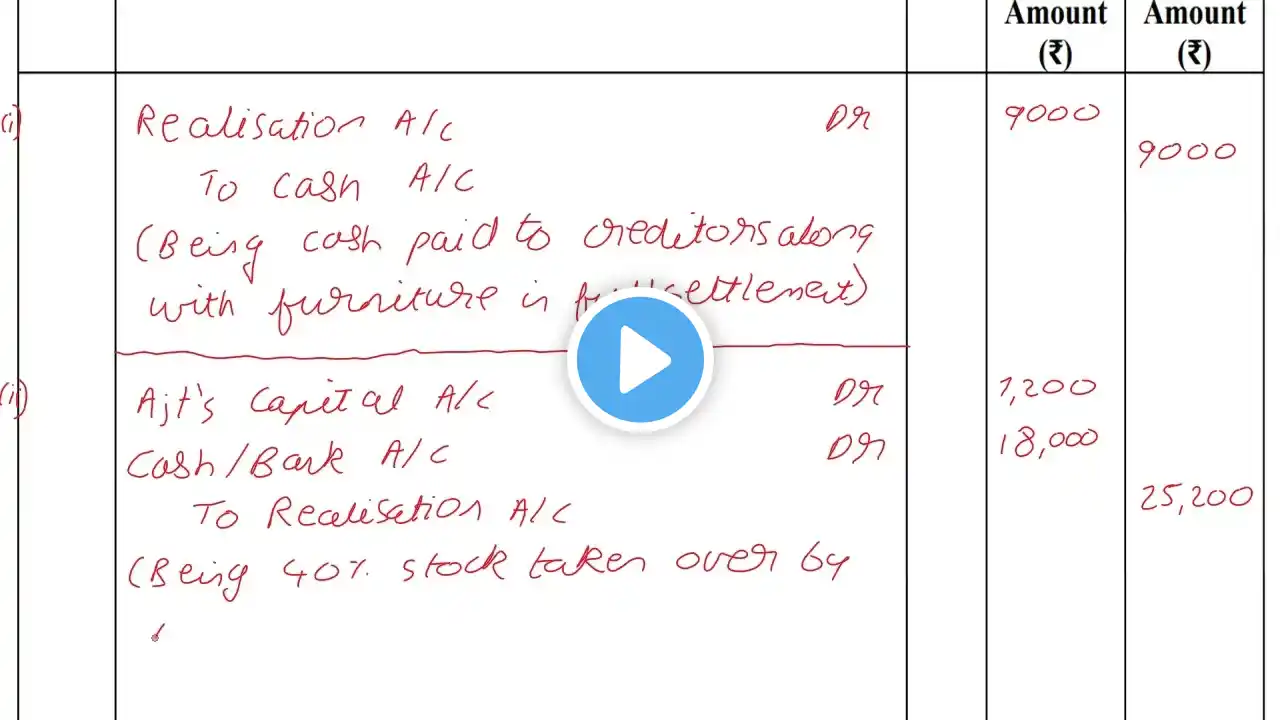

Pass the necessary journal entries for the following transactions on the dissolution of a partnership firm of Vibha and Ajit after various assets (other than cash) and external liabilities have been transferred to Realisation Account : (i) Creditors worth ₹ 46,000 accepted ₹ 9,000 cash and furniture of ₹ 32,000 in full settlement of their claim. (ii) The firm had stock of ₹ 20,000. Ajit took over 40% of the stock at a discount of 10% while the remaining stock was sold for ₹ 18,000. (iii) Vibha was appointed to look after dissolution work for which she was allowed a remuneration of ₹ 16,000. Vibha agreed to bear the dissolution expenses. Actual dissolution expenses ₹ 15,000 were paid by Vibha. (iv) Ajit’s loan of ₹ 45,000 was settled at ₹ 42,000. (v) A machine which was not recorded in the books was taken over by Vibha at ₹ 23,000, whereas its expected value was ₹ 28,000. (vi) The firm had a debit balance of ₹ 20,000 in the Profit and Loss Account on the date of dissolution.